Explaining Mutually Exclusive and Collectively Exhaustive ~ Where Did My Paycheck Go?

How your monthly budget can explain two core ideas from probability, risk, and economics ~

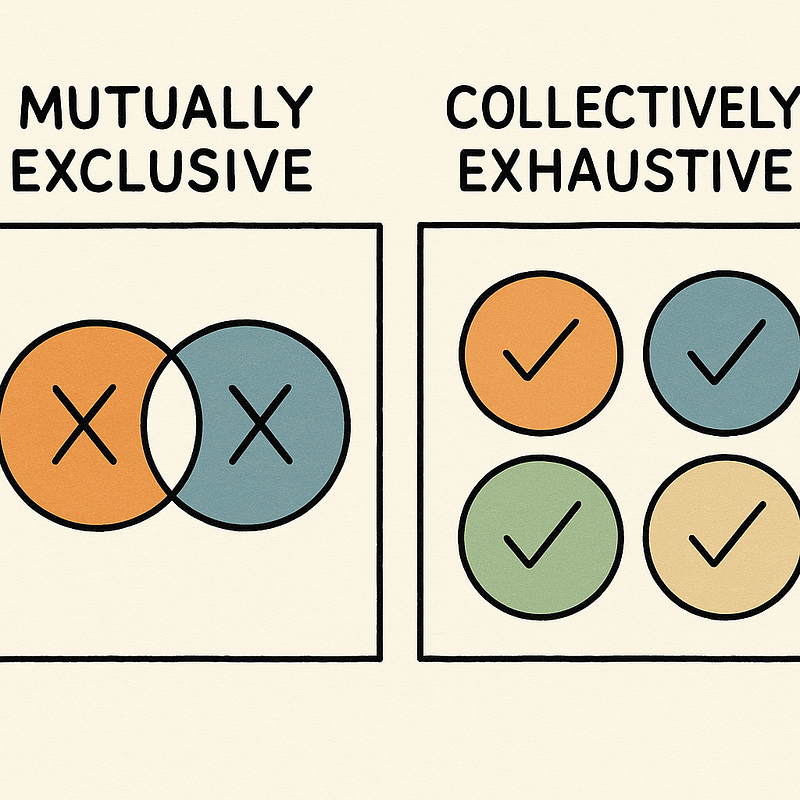

Mutual Exclusivity and Collective Exhaustion

Your paycheck hits your account on the first of the month.

For a brief moment, you feel rich!

Then your rent payment drops, credit cards auto-draft, a couple of deliveries arrive at your doorstep, and by the time you check again your balance is a lot smaller than you remember…

You ask the same question everybody asks ~

Where did all my money go?

That question isn’t just about money. It’s about categories.

You are trying to break one stack of cash into clean buckets: rent, food, gas, fun, savings.

Behind that exercise sit two phrases that sound like textbook trivia:

- Mutually exclusive

- Collectively exhaustive

They show up in probability, risk, and economics, but they also describe what you’re trying to do every time you build a budget.

Once you see them in that setting, things start making a lot more cents.

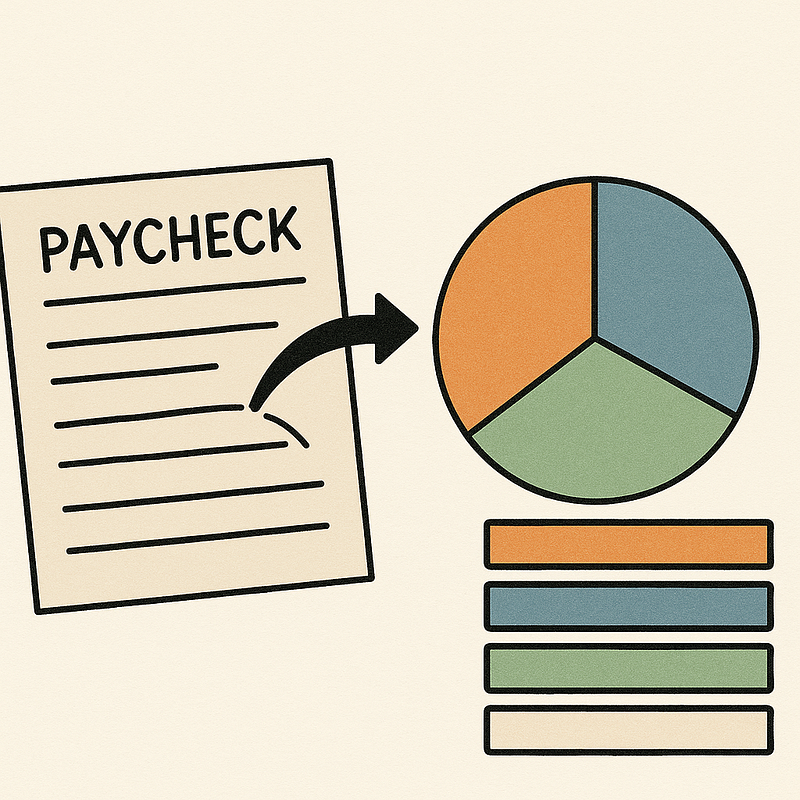

Building a Simple Paycheck Budget With Clear Spending Categories

Say you bring home $3,000.

You decide to track every dollar with a few broad categories.

Maybe you pick:

- Housing

- Groceries and household supplies

- Transportation

- Debt payments

- Subscriptions and monthly bills

- Fun and dining out

- Savings and investing

You pull up your bank history and begin dropping each transaction from last month into each of the buckets.

Even if you never say it out loud, you’re aiming for two things:

- Each dollar should land in one bucket, not several at once.

- Every dollar should land in some bucket, with nothing leftover.

Those two simple aims are the heart of the fancy terms

- Mutually exclusive ~ categories do not overlap for a single item.

- Collectively exhaustive ~ together, the categories cover every relevant part of the picture.

You already care about both ideas whenever you ask, “Where did it all go?” The math vocabulary just gives names to habits you are trying to build anyway.

Mutually Exclusive Categories: One Dollar, One Budget Bucket

Take the first idea: no overlaps.

You spend $18 at a restaurant on Friday night.

What is that?

You could call it food.

You could call it entertainment.

You might even call it mental healthcare.

If you aren’t careful, that single charge can sneak into more than one category. Part of it ends up in groceries, part in fun, and you tell yourself you invested in self-care.

On the statement, it’s one transaction. On your budget, who knows???

That is what it’s like when you fail the mutual exclusivity test. One dollar gets counted as if it belongs in multiple places. Your food spending looks higher than it really is. Your fun spending looks higher than it really is. Your self-care category too ~

The problem isn’t just cosmetic. Double counting mis-shapes the story. You might conclude you’re “investing heavily” in your well-being when in reality you just found three labels for the same night out.

The rule is simple:

One dollar, one bucket.

You can argue about which bucket a charge belongs in ~ that’s smart. Once you decide, keep it consistent and locked in.

That’s all “mutually exclusive” really means in this context.

Collectively Exhaustive Categories: Making Sure Every Dollar Is Counted

Now let’s look at the second idea: no gaps.

Suppose you finish sorting your month and total up the categories.

But something feels off.

Your take-home pay was $3,000, but your seven buckets only add up to $2,500.

There’s a $500 ghost in the machine ~

When that happens, you have just seen what it means for a list of categories to not be collectively exhaustive. Your set leaves out something…

Maybe you forgot:

- Cash withdrawals

- A one-off car repair

- An annual fee that hit this month

- A Venmo payment you mentally tagged as “we’ll square up later” and then forgot

Those dollars left your account.

Leaving them out of the list only hides where the money went.

A set of categories is collectively exhaustive when every relevant outcome has somewhere to land.

For a budget, that means every dollar shows up in exactly one place. For a risk or economics model, it means every cause or type of impact you care about has a box.

In real life, no list is perfect.

There is almost always an “Other” bucket. The goal is to keep that slice small and boring, not giant and mysterious.

If half your spending is in “Other,” you do not have a budget ~ you’ve got a shrug.

Common Budget Mistakes: Overlapping and Missing Categories

When you understand mutual exclusivity and collective exhaustion ~ no overlap, no gaps ~ you start noticing how often personal budgets fail both at the same time.

Imagine you decide to shrink “Fun and dining out” this month so you can build an emergency fund.

You track every restaurant meal and coffee shop visit carefully.

At the same time, you have a habit of buying snacks when you fill up gas. The receipt comes from Buc-ees, so you throw it into “Transportation.”

On paper, your fun spending drops. Your transportation category swells. You feel proud of your discipline and annoyed at the price of gas?

In reality, part of what you think of as “transportation costs” is just food hiding inside of fuel! Those two categories overlap in spirit, even if they don’t overlap in your brain.

That overlap points your frustration at your car instead of your snack habit.

Now flip to the other failure.

Suppose you skip “Subscriptions and small recurring charges” entirely because they feel trivial. No streaming services, no software, no cloud storage, no free trial that was never cancelled.

You ignore them because you hardly notice them.

Over a year, those silent charges add up to hundreds of dollars.

They never show up on the budget, but they definitely show up in your

account balance ~ quietly trickling out of the bank.

The budget is not collectively exhaustive. There’s a missing bucket, and that changes behavior. You might cut back on big obvious costs and overlook the slow leaks… but oversights like that add up, and quick!

Risk and economic models are vulnerable to the same pair of mistakes. Overlapping categories make some problems look bigger than they are. Missing categories make other problems vanish until they turn into a crisis.

Your Budget as a Model: How Category Design Shapes What You See

When you design categories for your own paycheck, you’re building a model of your financial life.

Every model makes choices.

You decide whether to combine “Housing” and “Utilities” or keep them separate. You decide whether a home coffee maker belongs in “Groceries,” “Fun,” or “Long-term savings” because it displaces café spending.

You decide whether to spread a yearly car insurance bill across the whole year or treat it as one heavy hit in the month it posts.

Those choices decide what patterns jump out at you.

Categories that are mutually exclusive and collectively exhaustive obey basic arithmetic.

The totals mean what they say.

You can misinterpret them, but at least the counting is honest.

If the categories overlap and leave big spaces uncovered, the patterns don’t mean anything! One month’s “transportation” balloons because snacks get lumped with fuel. Another month’s “fun” looks out of control because everything from tickets to takeout got jammed together.

And you’re left reacting to a mirage.

Analysts inside companies, banks, and agencies wrestle with this more than most people see. Their work might feed into decisions about credit, insurance, levee upgrades, or stimulus programs.

On the surface, it looks like a wall of charts. Behind the curtain, there’s a long (and often painful) debate about where to draw the lines.

Your own budget is smaller, but the same.

From Personal Budgeting to Economics and Risk Analysis

Once these ideas feel natural in your own money tracking, it becomes easier to see them in news stories and reports.

A few examples:

- A news article breaks the economy into “manufacturing, services, and everything else.” You can ask yourself: could the same dollar of output be counted in more than one of these? If so, the categories are not mutually exclusive. Is “everything else” huge? If so, the list is not very exhaustive.

- A company earnings report splits revenue into “domestic, international, and digital.” A single sale to a customer overseas through an app might be domestic to the firm, international by customer, and digital by channel. If that one sale can sit in several buckets, the totals by segment are trickier than they look.

- A risk assessment lays out three paths for next year: “baseline,” “upside,” and “downside.”

Ask yourself two questions:

- Could more than one of these happen at the same time?

- Do these three stories cover most of what might realistically occur, or are there missing pieces to the puzzle?

Those are the simple mutually exclusive and collectively exhaustive checks laid out in plain language.

Economists, actuaries, and risk specialists lean on these ideas when they shape scenarios, count losses, or assign probabilities. The terms sound formal, but in practice they’re the same two gut checks you use on your own budget: does anything double count? Did we leave anything out?

A Simple Rule for Mutually Exclusive and Collectively Exhaustive Thinking

If you want an easy way to remember, think about this:

Whenever you slice something into categories ~ money, time, causes, scenarios ~ ask yourself two questions.

- Does any single item clearly belong in more than one bucket at once?

- Does anything important have nowhere to go?

If the first answer is “no” and the second is also “no,” you’re in good shape.

Real life leaks around the edges, and you may keep a small “Other” bucket. That’s totally fine. The key is that you’ve made it harder for overlap and blind spots to distort the picture.

Seen that way, “mutually exclusive and collectively exhaustive” aren’t just textbook phrases ~ they’re habits of mind:

One dollar, one story, and no dollars missing.

And the next time you pull up your bank app and wonder where your paycheck went, you’ll have more than just a shrug. You’ll have a clearly carved pie and a better shot at being honest with yourself.