Generation Inflation

An Exploration

The Rising Costs of Financial Success

Imagine needing $600,000 a year just to feel financially secure. For Generation Z, this is not a lofty dream: it is the baseline. A recent survey found that younger Americans believe they need a net worth of $9.5 million to consider themselves successful, a stark contrast to the $1 million benchmark set by Baby Boomers (Empower, 2024). This gap is not just about generational optimism; it reflects the profound economic challenges younger generations face. Skyrocketing living costs, stagnant wages, and shifting cultural expectations have completely rewritten the rules of financial success.

This phenomenon, what we will call “Generation Inflation,” goes beyond rising prices. It encapsulates the harsh financial realities shaping the aspirations of younger generations. By examining the soaring costs of essentials, wage stagnation, and evolving perceptions of wealth, we can better understand the pressures facing Generation Z, and what these trends reveal about the future of the American economy.

The Impact of Intergenerational Inflation

To understand why younger generations feel financially behind, we need to look at inflation’s outsized role in shaping their reality. Over the past seven decades, the prices of essential goods and services have risen dramatically, far outpacing wage growth.

Consider the following:

In 1950, a loaf of bread cost $0.14. By 2023, that same loaf cost $3.00, a 2,043% increase (Bureau of Labor Statistics, 2023).

The cost of a new home surged from $14,500 in 1950 to $400,000 in 2023, a 2,659% increase (National Association of Realtors, 2024).

College tuition soared from just $600 per year in 1950 to $25,000 in 2023, a staggering 4,067% rise (NCES, 2024).

These increases reveal how the cost of achieving traditional milestones: homeownership, education, and financial independence, has become a heavier burden for each successive generation.

Even as nominal wages have risen, the reality is that purchasing power has eroded. Essentials like housing, education, and healthcare now consume a significantly larger share of household income, forcing Generation Z to set higher financial goals simply to achieve the same standard of living their parents enjoyed.

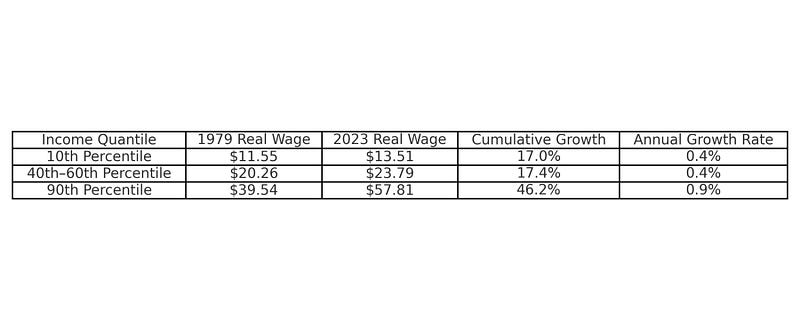

Stagnant Real Wage Growth

While the cost of living has skyrocketed, wages have failed to keep pace, particularly for middle- and lower-income workers. When adjusted for inflation, real wages reveal a troubling stagnation.

Between 1979 and 2023, workers in the 10th percentile of earnings saw just a 17% increase in real wages, equivalent to an annual growth rate of only 0.4%. Even those in the middle (40th-60th percentile) experienced similarly meager gains. In contrast, the wealthiest workers in the 90th percentile saw a more substantial rise of 46.2%, reflecting widening wage inequality (Visual Capitalist, 2023).

This stagnation hits younger generations especially hard. They face steeper costs for housing, education, and healthcare, but median wages haven’t kept up. As a result, achieving financial stability is significantly more challenging for Generation Z than it was for Baby Boomers at the same life stage.

Perceptions of Wealth and Success

The widening gap between costs and wages has fundamentally reshaped how younger generations view wealth. For Generation Z, aspiring to $600,000 a year in income is not about luxury: it is about survival in an economy where traditional milestones like buying a home or paying off student loans demand significantly more resources.

Social media and influencer culture compound these anxieties. Platforms like Instagram and TikTok showcase lifestyles of unattainable luxury, creating a constant comparison trap. Even those earning well above the median may feel “behind,” as success becomes increasingly defined by a curated ideal.

Additionally, macroeconomic factors like the rapid expansion of the U.S. money supply and mounting federal debt undermine confidence in long-term financial stability. For Generation Z, these cultural and economic dynamics converge to make wealth feel urgent yet unattainable.

The Dollar as Fiat Currency

Exacerbating these challenges is the dollar’s status as a fiat currency, which relies on trust and government policy rather than tangible assets like gold. Over the past few decades, the U.S. has dramatically expanded its money supply (M2) to stimulate growth and address crises like the Great Recession and the COVID-19 pandemic.

While these policies have prevented economic collapse in the short term, they contribute to inflation and erode the dollar’s purchasing power over time. Younger generations are left navigating an economy that feels increasingly precarious, where financial success requires constant adaptation to shifting economic realities.

Conclusion: The Cost of Generation Inflation

For Generation Z, financial aspirations like earning $600,000 a year or building a $9.5 million net worth may seem excessive to older generations. But in today’s economy, these numbers represent the minimum required to navigate rising costs, stagnant wages, and an unpredictable financial landscape.

If inflationary pressures and wage stagnation persist, financial security will remain out of reach for many younger Americans. Addressing these systemic barriers requires innovative policy solutions: investing in wage growth, reining in the costs of essentials, and promoting long-term financial stability. Until then, Generation Z may find that their lofty financial goals are less about excess and more about survival in an era of “Generation Inflation.”

Works Cited

Empower. “Survey on Generational Perceptions of Financial Success.” 2024.

New York Post. “Baby Boomers and Financial Aspirations.” 2024.

Bureau of Labor Statistics. “Historical Consumer Price Index Data.” 2023.

National Center for Education Statistics (NCES). “Trends in College Costs.” 2024.

Visual Capitalist. “Real Wage Growth by Income Quantile, 1979-2023.” 2023.

National Association of Realtors. “Median Home Prices by Year.” 2024.