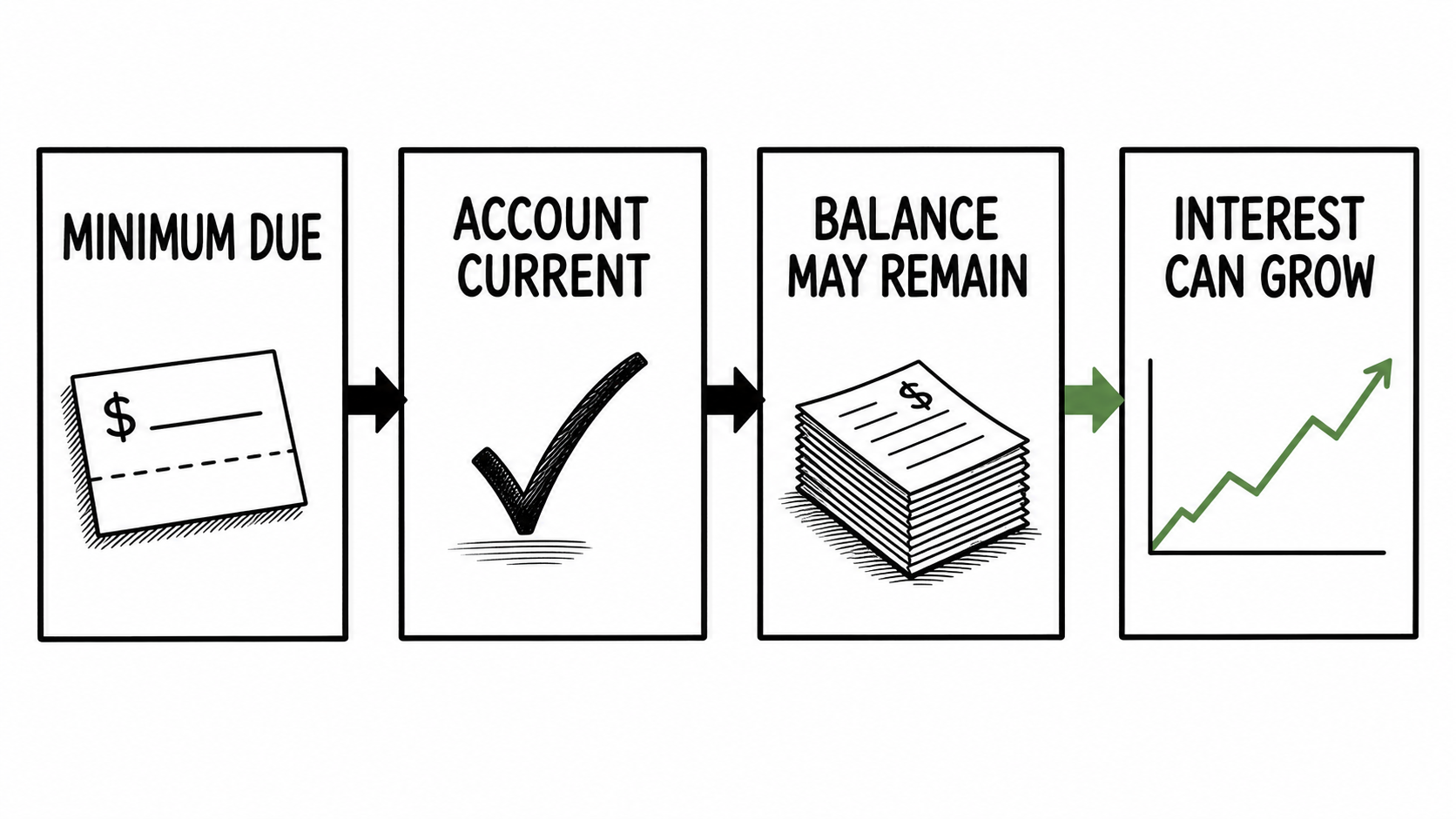

Minimum Due

The smallest allowed payment isn't the full price.

Minimum due sounds like a bill getting smaller. It isn’t. It names the smallest door you can walk through this month without being late.

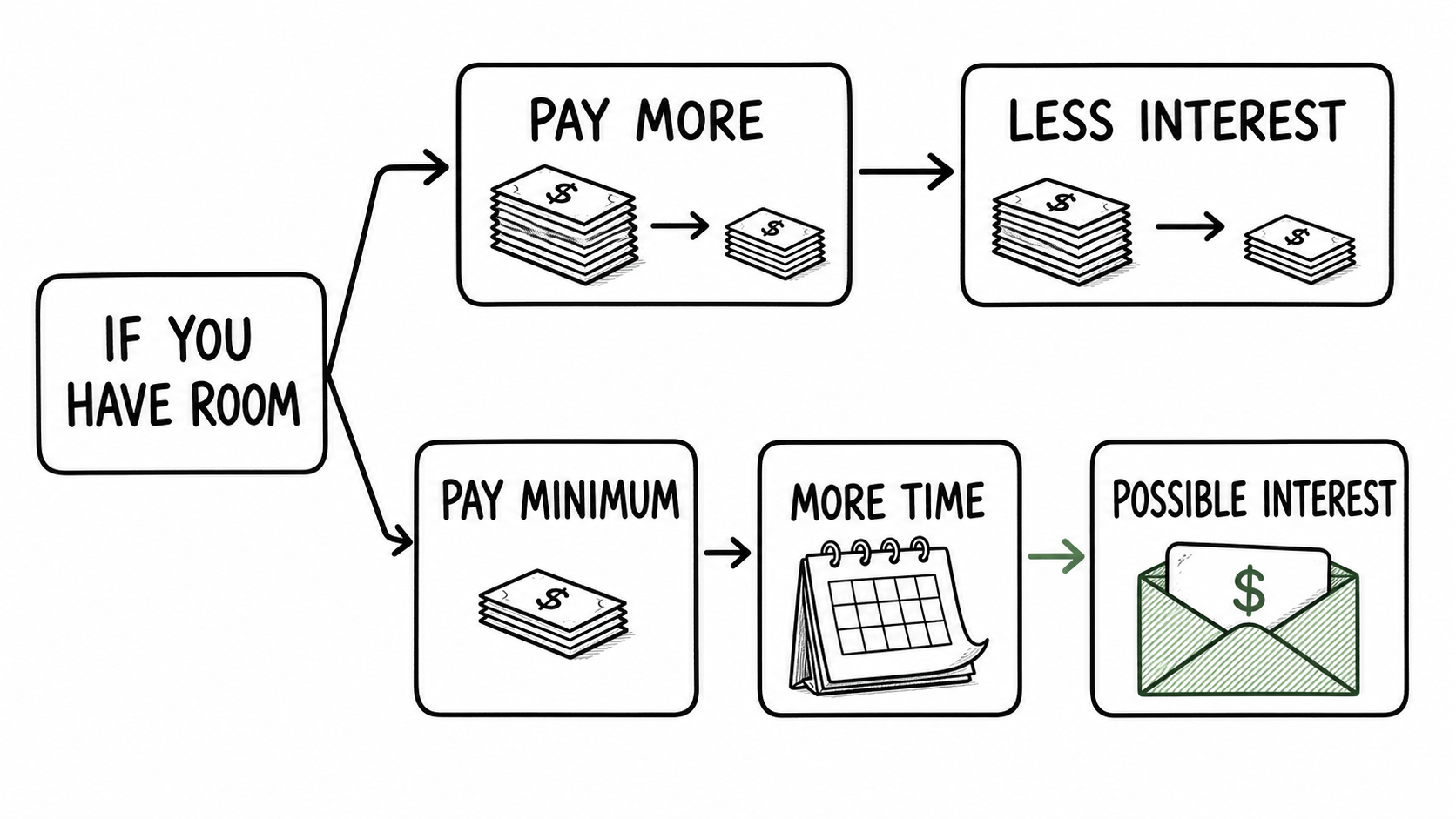

The CFPB tells consumers they don’t have to pay more than the minimum shown on a credit-card statement. It also says paying more each month means paying less interest over time. If a person pays only the minimum, the debt could take years to clear.

Federal disclosure rules point the same way. Regulation Z requires credit-card statements to show repayment estimates tied to minimum payments and assumptions about no new amounts added to the balance. The law puts that little box on the page because the floor needs a warning sign.

The minimum can keep the account current while the balance may remain.

The Small Door

The smallest door isn't the whole road.

Sometimes the minimum is all a person can pay. A lost shift, a medical bill, or a broken car can turn the floor into the only reachable step. The honest rule has to leave room for hard months. No honest ledger should sneer at that.

But when there is room to choose, the word minimum needs to be understood correctly. The lender may keep earning. The purchase may remain partly unpaid. The account can stay current while the balance keeps growing and growing.

That price often moves: next month, next paycheck, future patience, future choices. The card company doesn’t need to shout. The statement already says the floor. The interest does the rest.

More than the minimum can lower interest; the minimum can buy time.

Ask this question at the kitchen table: am I paying the bill, or buying more time with the bill? One answer lowers the balance. The other rents another month. The minimum can keep trouble away for a month. It will never make the debt disappear. When the cost is hidden behind the smallest allowed payment, your future self ends up paying the price.