Smokestack Spreadsheets

OpenAI's missed targets turned a private forecast into a public wager on chips, cloud contracts, substations, and time.

The Forecast Tab

The object at the center of the April 28 AI selloff was probably a forecast tab.

No stage demo. No new model card. No keynote screen showing a chatbot writing code under studio lights. The thing that moved markets was more ordinary: internal targets for users and revenue, the kind of numbers that live in rows, dates, assumptions, and conditional formatting.

On April 28, The Wall Street Journal reported that OpenAI had missed several internal revenue and user-growth targets, including an internal goal for ChatGPT to reach one billion weekly active users by the end of 2025. The Journal also reported that Chief Financial Officer Sarah Friar had raised concerns internally about whether sales growth could support the company’s future computing needs.

That last phrase changed the air around the report. A normal startup miss damages a valuation story. A frontier-AI miss touches factories, chips, power contracts, cloud partners, utility queues, and public companies whose own value has been built around demand for AI infrastructure.

The link showed up quickly in public markets. The Associated Press reported that AI stocks helped pull Wall Street lower on April 28 after the Journal report raised concern inside OpenAI about the cost of data centers after missed user and revenue targets. Broadcom, Nvidia, and Micron fell that day. Kiplinger reported that Oracle, CoreWeave, AMD, Broadcom, and other AI-linked names also sold off under the same pressure.

The reaction may have looked excessive. A missed target is not the same thing as failure. Private targets can be ambitious by design. A missed user goal can leave a company with a large base. Revenue can lag demand during a buildout. Investors overreact during crowded trades.

All of that can be true, and the forecast can carry weight.

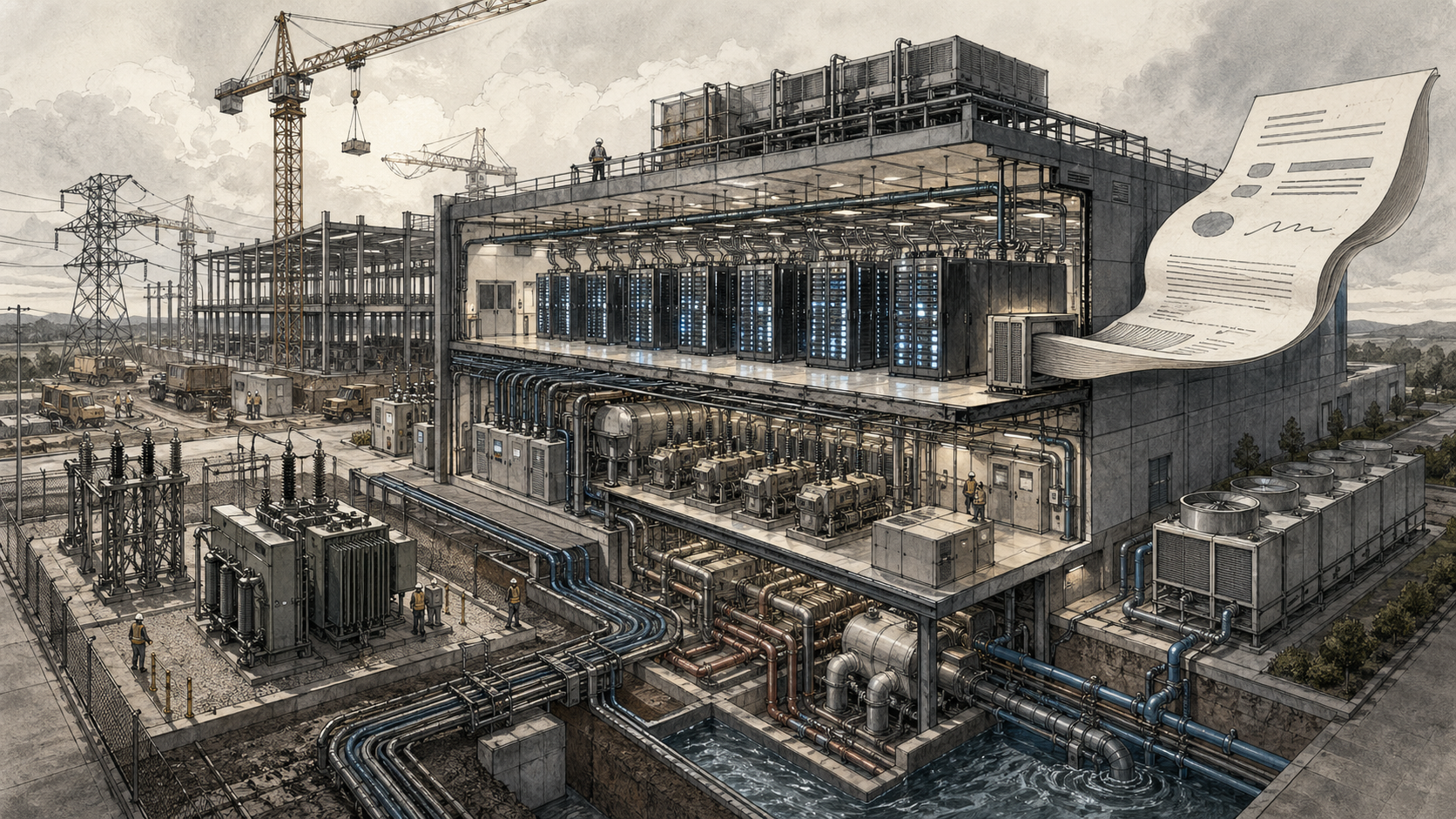

The spreadsheet is useful because it names the hinge. Frontier AI has become an industry where revenue growth has to arrive in time to pay for physical scale. The model may feel weightless to the user. The bill arrives in steel, silicon, concrete, cooling loops, substations, debt, equity, and long cloud contracts.

Compute as a Promise

OpenAI’s most visible product is software. Its binding constraint is industrial.

A query enters a chat window. Behind it sits a large chain of facilities and suppliers: chips, memory, servers, network gear, data halls, power equipment, backup generation, cooling, fiber, land, permits, and labor. Training a frontier model requires a large concentration of that machinery. Serving millions of users requires a second kind of scale, less cinematic and more relentless. The system has to answer every hour.

That is why compute is more than an expense line. For a frontier-AI company, compute is the promise that the next product will exist, the present product will stay responsive, and the business will keep gaining users before rivals catch up.

OpenAI’s public cloud arrangements show how central capacity and distribution have become. On April 27, Microsoft announced a revised OpenAI agreement in which Microsoft remains the primary cloud partner, OpenAI products ship first on Azure under certain conditions, and OpenAI can serve products through any cloud provider. Microsoft’s OpenAI license is now non-exclusive through 2032, and the companies reworked revenue-share terms.

The next day, AWS announced that Amazon Bedrock would offer OpenAI models, Codex, and managed agents in limited preview. That announcement sounds technical, but it also tells a business story. Those arrangements give OpenAI more routes to customers, more compute options, and more ways to turn model capability into paid work.

The business risk is not simply that compute is expensive. It is that capacity has to be arranged before revenue is fully proven. A cloud commitment can look prudent when demand is rising and heavy when growth slips. That is the difference between buying a variable input and reserving an industrial system.

Cloud contracts serve two masters. They secure capacity for growth. They also create obligations that expect growth. The same contract that reassures a product team can make a finance team sweat if adoption slows, churn rises, or enterprise spending takes longer to close.

That is the risk structure now. The company signs for the capacity it believes the future will require. The future arrives in monthly revenue, user retention, and customers who may be testing tools before committing core work to them. The gap can be filled with capital for a while. Capital has a mood. Construction schedules do not.

The Power Plant Behind the Demo

The deeper story is power.

Investors talk about AI as a software market because that is how the revenue appears: subscriptions, API calls, agents, enterprise seats, developer tools. The buildout underneath eats like heavy industry.

The International Energy Agency’s latest AI-energy work gives the scale. In a new report notice published in April 2026 , the IEA said capital spending by five large technology companies rose above $400 billion in 2025 and is set to rise another 75 percent in 2026, driven by data center investment. The agency said data center electricity demand rose 17 percent in 2025, and electricity use by AI-focused data centers rose faster. It also warned that data center expansion is running into bottlenecks in chips, gas turbines, transformers, planning systems, regulatory approvals, and grid connections.

The U.S. Energy Information Administration has described the domestic grid version of the same problem. In March, EIA said ERCOT and PJM are expected to see the fastest growth in electricity demand tied to data centers through 2027, with additional growth in regions managed by MISO and SPP and in Arizona and Nevada. EIA’s high-demand scenario showed natural gas generation doing much of the extra work, with wholesale power prices rising most sharply in Texas.

The older Department of Energy baseline remains useful. DOE’s 2024 data center report, summarized by the department, estimated that U.S. data centers used about 4.4 percent of national electricity in 2023 and could consume 6.7 percent to 12 percent by 2028.

These figures change the meaning of an AI growth target. A user forecast is also a load forecast. A revenue target is also a power procurement question. A cloud partnership is also a bet about substations, transmission, transformers, fuel, and local politics.

That can be hard to see because AI arrives in polite boxes on a screen. It feels like a new layer of language. The physical layer hides behind the interface until the interface needs more capacity than the grid can deliver on schedule.

Then the demo asks for a power plant.

The model runs inside a contract, a substation, a cooling loop, and a construction schedule.

The model runs inside a contract, a substation, a cooling loop, and a construction schedule.

The Public Edge of a Private Forecast

OpenAI is private. Its internal targets are private. Its missed goals are, in one sense, a problem for executives, employees, investors, and business partners.

The public edge appears because the buildout is no longer contained inside the company.

Data centers need sites. They need local permits, water systems in some places, new substations, transmission upgrades, backup power, and generation contracts. They sit near communities that may receive jobs and tax base, then also receive noise, land-use conflict, power-price anxiety, water questions, and emergency planning problems. Utilities must decide how much capacity to build for a customer class whose demand curve is racing ahead of old planning habits.

This is why the OpenAI miss rippled into public stocks. Oracle, CoreWeave, Nvidia, AMD, Broadcom, and other companies are part of a larger belief about AI demand. Their own revenue stories depend on the idea that frontier models will need more chips, more cloud capacity, more servers, and more specialized facilities. A private forecast at the center of that belief can shake public balance sheets.

Households and businesses also sit in the electricity system underneath those balance sheets. If data center demand arrives faster than new supply, someone has to absorb the strain. Sometimes that means higher wholesale prices. Sometimes it means new gas plants, delayed retirements, transmission fights, or rate structures designed to protect households. Sometimes it means a large customer builds or contracts for its own power, then communities argue over land, water, emissions, wires, and who benefits.

That does not mean households automatically subsidize every data center. Rate design, interconnection agreements, power-purchase contracts, utility commission decisions, and local tax arrangements matter. But it does mean the cost question leaves the company’s spreadsheet and enters public utility planning.

A live example is already visible in the utility business. Reuters reported that Entergy had raised its four-year capital spending plan to serve large data-center demand tied to Meta in Louisiana, including seven planned gas-fired power plants totaling more than 5.2 gigawatts. The company says the arrangement is structured so data centers pay more rather than shifting the burden onto ordinary customers. That is exactly the point. The public question is not whether data centers always impose costs on households. The question is who writes the contract, who approves the rate structure, who builds the plant, and who is left exposed if the forecast changes.

None of this makes AI uniquely suspect. Railroads, steel, oil, autos, telecom, and the early internet all tied private fortunes to public infrastructure. The problem is less novelty than speed. Frontier AI has compressed an industrial buildout into a financial narrative that expects software-like growth.

That compression gives every forecast more work to do.

The Patience Problem

The AI buildout needs patient capital. It has been receiving impatient attention instead.

Public markets like the story of massive demand. They like the supplier chain when revenue appears. They like a private company that can justify enormous chip orders, power deals, and cloud commitments. They also turn quickly when one of the central buyers appears to need more time.

The irony is that infrastructure rarely respects venture rhythm. Data centers, transmission lines, substations, turbines, and transformers are slow. Power markets clear on their own calendars. Local hearings can stall a site. Equipment lead times can stretch across years. A model race asks for speed; the grid answers in queue numbers.

That is a duration mismatch. The revenue question resets every month. The infrastructure commitment can last for years. A product team can change a roadmap in a quarter. A utility cannot unbuild a substation because enterprise adoption came in light.

That mismatch creates pressure inside OpenAI and around it. If the company buys too little compute, rivals gain room. If it buys too much, future revenue has to catch up. If it spreads work across cloud partners, it gains capacity and reach, then accepts more complexity. If it slows the buildout, the market may read discipline as weakness. If it accelerates, the market may read ambition as a bubble.

The company is trying to manage a product curve, a capital curve, and a power curve at the same time.

The hard part is that each curve has a different judge. Users judge usefulness. Enterprise customers judge reliability, security, cost, and fit with existing systems. Investors judge growth and margins. Utilities judge load. Local governments judge land and public cost. Competitors judge speed. None of those judges owes the others patience.

What the Miss Measured

A missed target can measure many things.

It can measure overconfidence. It can measure slower enterprise adoption. It can measure competition from Anthropic, Google, xAI, open models, or in-house tools. It can measure churn, pricing friction, capacity constraints, product confusion, procurement caution, or simple forecasting error. It can also measure a market trying to learn how fast a new general-purpose technology becomes ordinary work.

That last measurement is the one worth keeping.

The optimistic case is not foolish. Enterprise adoption often starts slowly, then hardens into ordinary workflow. Inference costs can fall. Better products can create uses that are hard to see from the first generation of tools. A company that looks overbuilt in one quarter can look prepared a few quarters later if demand catches up.

The AI argument has spent years trapped in two cramped stories: instant overnight change and empty bubble. The real system is more demanding than either story. AI can be genuinely useful while struggling to fund its industrial footprint at the speed investors want. A company can have extraordinary technology and face ordinary arithmetic. A model can answer in seconds and depend on equipment that takes years to build.

The OpenAI report matters because it brought those clocks into one view. The user clock, the revenue clock, the compute clock, the construction clock, the grid clock, and the investor clock all started ticking in public.

The industry will try to explain the miss away. It may point to new models, bigger partnerships, stronger enterprise demand, cheaper inference, better chips, or fresh capital. Some of those answers may prove real. The cost per task could fall. Better products could deepen demand. Multi-cloud distribution could turn capacity into revenue more cleanly. The forecast may look different a quarter later.

But the basic question will remain.

How much physical world does frontier AI need before the money arrives, and who carries the cost if the timing slips?

A private miss becomes public when the bill touches markets, utilities, and the grid.

A private miss becomes public when the bill touches markets, utilities, and the grid.

The World the Spreadsheet Asked For

The forecast tab is easy to underrate because it is bland. It has no moral drama on its face. A cell is green or red. A month is ahead or behind. A goal is met or missed.

Yet a forecast is a claim on the world. It says users will arrive, customers will pay, power will be available, chips will ship, facilities will open, contracts will hold, investors will wait, and local systems will absorb the demand.

That is a large claim for a small tab.

OpenAI’s missed targets did not end the AI buildout. They made its terms more visible. The frontier is no longer confined to a lab, a chat window, or a model leaderboard. It runs through cloud contracts, bond markets, earnings calls, substations, power plants, utility commissions, and communities deciding what kind of industrial neighbor a data center will be.

The spreadsheet was small. The world it asked for was enormous.