The National Flood Insurance Program

An Exploration

A Precarious Future Amid Rising Costs

Flooding is the most costly natural disaster in the United States, causing billions in damages annually. However, the very program designed to insure against this risk – the National Flood Insurance Program (NFIP) – is $20 billion in debt and struggling to survive (FEMA, 2024). Created in 1968 to provide affordable flood insurance for property owners in flood-prone areas, the NFIP has become financially unsustainable, burdened by mounting debt, outdated risk assessments, and escalating claims fueled by climate change.

Climate change compounds these challenges, increasing the frequency and severity of floods while encouraging development in high-risk areas. As the program struggles to remain viable, it has inadvertently created a cycle that places communities, taxpayers, and the environment at greater risk. This article argues that the federal government must phase out NFIP coverage for high-risk areas, redirecting resources to incentivize climate-resilient development.

The NFIP’s Financial Insolvency

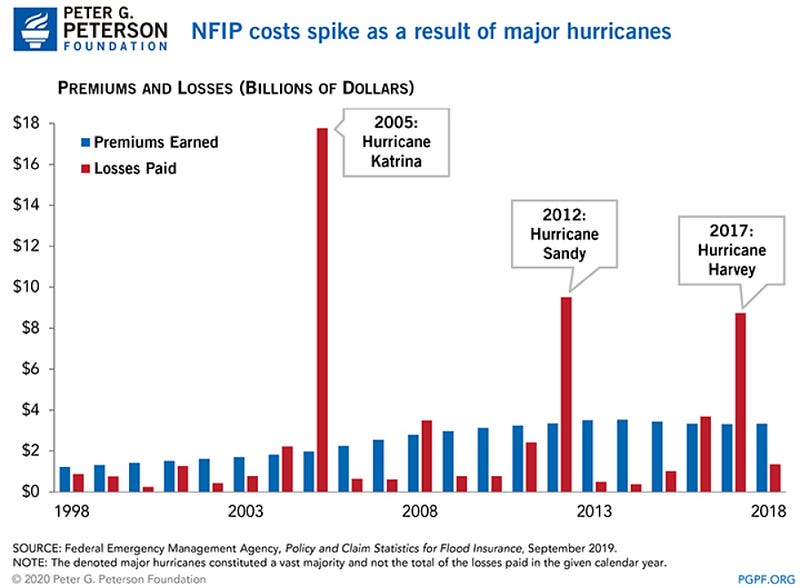

The NFIP’s financial condition has deteriorated significantly over the past several decades. The program is burdened with a $20 billion debt to the U.S. Treasury, highlighting the systemic mismatch between its revenue from premiums and its liabilities (FEMA, 2024). The situation worsens during years of catastrophic flooding, when claims far exceed the program’s financial capacity.

Major disasters like Hurricane Katrina (2005) and Superstorm Sandy (2012) overwhelmed the NFIP, requiring massive federal loans to keep the program afloat (CRS, 2024). Even in less catastrophic years, the program struggles under the weight of escalating payouts.

The NFIP currently insures 4.7 million properties, with the average insured home valued at over $300,000 (House Financial Services, 2024). Altogether, that’s a staggering $1.41 trillion in insured value – far exceeding the program’s ability to cover potential losses. Yet premiums often fail to reflect the true risk of these properties.

Outdated FEMA flood maps, which determine premiums and risk zones, are a major culprit. These inaccuracies result in underpriced policies that leave the NFIP chronically underfunded. Subsidized premiums for high-risk properties further exacerbate this funding gap, perpetuating the program’s reliance on taxpayer bailouts.

Rising Costs Due to Climate Change

The financial pressures on the NFIP will only intensify as climate change accelerates flooding risks. Research shows that one-third of historical flood damages in the United States are attributable to climate-driven changes, such as heavier precipitation and rising sea levels (Stanford, 2021).

Climate-Driven Flood Risks

- Rising sea levels: Coastal communities face increasingly severe storm surges and tidal flooding, making them more vulnerable to high-value losses.

- Heavier rainfall: Inland areas are experiencing more frequent and intense flash floods, driven by shifting precipitation patterns.

- Recurring disasters: 1-in-100-year floods are now occurring in some regions every decade.

By 2050, even under moderate climate scenarios, annual flood damages are projected to increase by 26% (Stanford, 2021). The NFIP, originally designed to address historical flood patterns, is ill-equipped to manage the compounding effects of climate change.

Adding to the program’s challenges is the fact that subsidized premiums encourage development in flood-prone areas. Repeated claims from these high-risk properties account for a disproportionate share of payouts, creating a vicious cycle of debt and escalating liabilities (Princeton, 2024).

In flood-prone areas like coastal Louisiana or the suburbs of Miami, families rely on NFIP insurance to rebuild after disasters. But as climate change worsens flooding, the program’s ability to protect these communities is stretched dangerously thin.

Phasing Out the NFIP in High-Risk Areas

The federal government must take decisive action to phase out NFIP coverage for high-risk areas. Continuing to subsidize flood insurance in these zones not only perpetuates unsustainable development but also exposes taxpayers to ever-growing financial risks.

Benefits of Phasing Out NFIP Coverage in High-Risk Areas

Reducing federal liability

By limiting NFIP coverage to areas with lower flood risks, the program can significantly reduce its financial exposure. This approach would help stabilize the NFIP and decrease reliance on taxpayer-funded bailouts.

Discouraging risky development

Without federally subsidized insurance, developers and homeowners would face market-driven costs that reflect the true risks of building in flood-prone areas. This would naturally disincentivize risky construction and promote sustainable land-use practices.

Encouraging resilient development

Redirecting federal resources to incentivize development in safer, climate-resilient locations could foster economic growth while reducing disaster recovery costs. Programs offering relocation grants or tax incentives could help communities transition away from high-risk zones.

Princeton’s research reinforces these points, noting that subsidized insurance undermines resilience by masking the true financial and environmental costs of building in flood-prone areas (Princeton, 2024).

A Model for Change: Redirecting Resources

Phasing out the NFIP in high-risk areas does not mean abandoning vulnerable communities. Instead, federal resources could be better used to:

- Provide relocation assistance: Offer grants to help property owners move to safer areas.

- Support infrastructure improvements: Invest in resilient infrastructure, such as levees and flood-resistant housing, in lower-risk zones.

- Implement zoning reforms: Encourage sustainable development through stricter zoning laws in flood-prone areas.

Conclusion

The National Flood Insurance Program is at a critical crossroads. Burdened by debt, outdated risk assessments, and mounting liabilities from climate change, the NFIP is no longer sustainable in its current form. Reform is not just necessary – it is fiscally and environmentally imperative.

Ending federally subsidized flood insurance in high-risk areas would reduce the program’s financial liabilities, discourage unsustainable development, and pave the way for more resilient land-use practices. By redirecting resources toward incentivizing climate-resilient development, the federal government can protect taxpayers, reduce disaster recovery costs, and promote a sustainable future.

Works Cited

- Federal Emergency Management Agency (FEMA). “NFIP Debt.” Accessed December 2024. https://www.fema.gov/case-study/nfip-debt .

- Congressional Research Service (CRS). National Flood Insurance Program Overview. Accessed December 2024. https://crsreports.congress.gov/product/pdf/IN/IN10784 .

- House Financial Services Committee. National Flood Insurance Program FY25 Letter. Accessed December 2024. https://democrats-financialservices.house.gov .

- Stanford University. “Climate Change Caused One-Third of Historical Flood Damages.” Stanford News. Accessed December 2024. https://news.stanford.edu/stories/2021/01/climate-change-caused-one-third-historical-flood-damages .

- Princeton University. “Overcoming Contemporary Reform Failure of the National Flood Insurance Program.” Journal of Public and International Affairs. Accessed December 2024. https://jpia.princeton.edu/news/overcoming-contemporary-reform-failure-national-flood-insurance-program-accelerate-just-climate .