The Strait That Holds the Price

Iran's Hormuz proposal shows how a narrow sea passage can turn war, fuel, shipping, fertilizer, and household prices into one shared line.

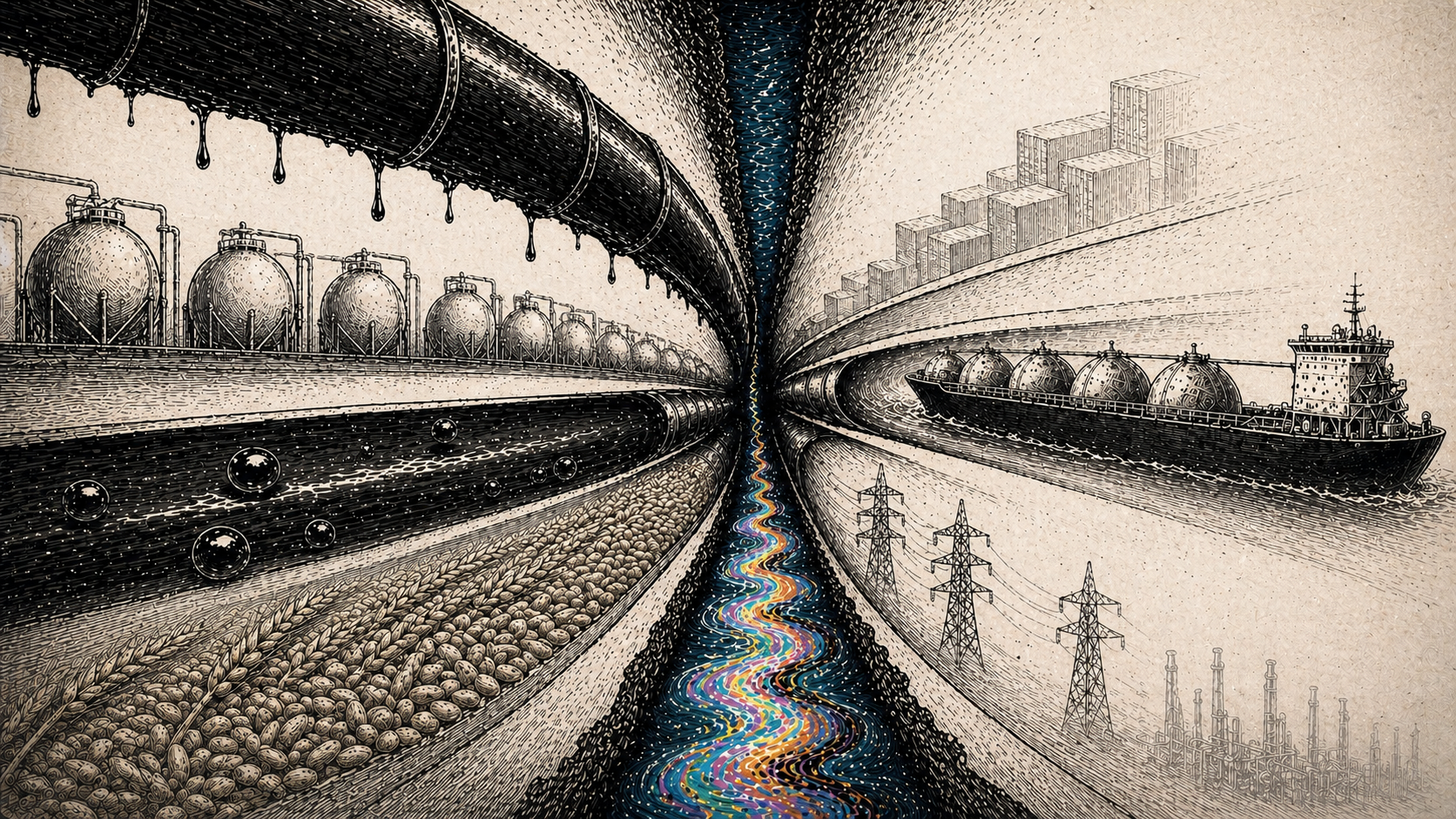

The Waterway

On a map, the Strait of Hormuz looks almost too small for the power assigned to it.

It is a seam of water at the mouth of the Persian Gulf. Oman sits on one side of the approach. Iran sits on the other. At its narrowest point, the International Energy Agency says , the passage is 29 nautical miles wide. The inbound lane and the outbound lane are each only two miles wide, with a buffer zone beside them.

The geometry is plain. The consequences take longer to surface.

A tanker leaving Gulf crude terminals has to move through that opening before it can reach the Arabian Sea. A liquefied natural gas cargo sailing out of Qatar faces the same fact. So do shipments tied to petrochemicals, fertilizer, plastics, jet fuel, diesel, and cooking gas. The strait functions as infrastructure without the reassuring look of infrastructure. No bridge. No dam. No control room. Just water, shoreline, and the disciplined spacing of vessels carrying much of the modern economy in their hulls.

Iran’s latest offer reaches beyond the diplomatic news cycle.

On April 27, the Associated Press reported that Iran had offered to reopen the strait if the United States lifts its blockade and ends the war, while pushing nuclear-program talks into a later phase. The same report said the United States appeared unlikely to accept a deal that leaves the nuclear issue unresolved. Secretary of State Marco Rubio publicly framed any agreement around preventing Iran from moving toward a nuclear weapon.

The proposal may fail. The details may shift. Another channel of talks may open through Pakistan, Oman, Russia, or direct phone calls. Yet the event has already done its work. It has shown, with unusual clarity, that modern economies can be forced back to the oldest kind of political problem: a narrow passage, a ship in waiting, and two sides trying to decide who can bear more pain.

The Chokepoint Under the Economy

The usual language of energy security can make the system sound abstract. Supply. Demand. Spare capacity. Risk premium. Futures curve. Inventory. Strategic reserve.

Hormuz strips away some of that language. The question becomes physical. How many barrels can pass? How many tankers are waiting? Which ports fill up first? Which pipeline can bypass the water, and how much can it really carry under stress?

The numbers explain why the strait keeps reappearing in every serious discussion of energy risk. The IEA’s February 2026 factsheet estimated that about 20 million barrels per day of crude oil and oil products moved through Hormuz in 2025, equal to roughly a quarter of world seaborne oil trade. The same factsheet said almost 20 percent of global liquefied natural gas exports also depend on the passage, largely cargoes tied to Qatar and the United Arab Emirates.

The U.S. Energy Information Administration made the older baseline even clearer. In 2024, EIA estimated that petroleum flows through Hormuz averaged 20 million barrels per day, about 20 percent of global petroleum liquids consumption. EIA also estimated that one-fifth of global LNG trade moved through Hormuz in 2024, primarily cargoes tied to Qatar .

The United States is less directly dependent on Gulf crude than it was decades ago. Domestic production and Canadian imports have changed the American exposure. EIA estimated that U.S. crude and condensate imports through Hormuz accounted for about 7 percent of total U.S. crude and condensate imports in 2024 and about 2 percent of U.S. petroleum liquids consumption.

That narrower exposure can produce a misleading comfort. Oil prices are global. Diesel markets are global. LNG cargoes chase the highest delivered price. A disruption near Qeshm Island can show up in a farmer’s fertilizer bill, a trucking company’s diesel invoice, an airline’s fuel hedge, a power plant’s gas contract, and a family’s grocery receipt. The United States can import less Gulf oil and live inside the price system that Hormuz disturbs.

The Spare Route Problem

Every chokepoint invites a search for bypasses.

In this case, the bypasses exist, but they leave much of the problem intact. Saudi Arabia has the East-West crude oil pipeline ending at Yanbu on the Red Sea. The United Arab Emirates has a pipeline ending at Fujairah outside the strait. The IEA estimates 3.5 to 5.5 million barrels per day of potential crude redirection capacity through those alternative routes. EIA’s 2025 analysis put available Saudi and UAE bypass capacity near 2.6 million barrels per day under the conditions it examined.

Those are large numbers until they are placed beside the flow they would need to replace. The IEA’s 2025 Hormuz oil total was just under 20 million barrels per day. A few million barrels of rerouting can reduce damage. The waterway remains central.

The same problem is sharper for LNG. Qatar and the UAE send almost all of their LNG exports through Hormuz, except deliveries bound for Kuwait. The IEA’s 2026 factsheet described the alternative route problem for Gulf LNG in blunt terms: cargoes need existing liquefaction facilities, and those facilities sit inside the geography that the strait controls.

This is where the diplomatic story turns into an infrastructure story. Decades of investment can build wells, terminals, storage tanks, pipelines, refineries, and fleets. All of that capital has to obey the last mile of geography. A system can become enormous and remain vulnerable at one small opening.

Scale creates that vulnerability.

The modern energy system is built around large assets, long routes, high use, tight timing, and cargoes that move because the channel stays open. The price advantage comes partly from that concentration. So does the weakness. A dispersed system costs more in ordinary times. A concentrated system can look lean until the queue stops moving.

Pain as Policy

The Hormuz standoff has made pain into a bargaining instrument.

Iran’s offer links the waterway to the U.S. blockade and the war. The United States, according to AP, wants any deal to address the nuclear program. Iran wants the strait and blockade treated first. The bargain turns on sequencing: which pressure comes off now, which question waits, and which side has to concede that its strongest instrument has reached its limit.

That sequencing question is not diplomatic housekeeping. It is the substance of the conflict.

For Iran, the strait is one of the few tools that can make distant consumers feel the war. Its military position may be battered. Its economy may be under enormous pressure. Yet geography gives Tehran a lever short of regional dominance. It requires the capacity to make passage uncertain.

For Washington, the blockade is an attempt to turn economic pressure inward on Iran. If Iranian crude cannot move, revenue dries up and storage fills. EIA’s April 2026 Short-Term Energy Outlook described the production consequences of limited Hormuz flows. The agency estimated that Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively shut in 7.5 million barrels per day of crude oil production in March, with April shut-ins expected to rise to 9.1 million barrels per day.

Those figures show how quickly a pressure campaign can spread beyond its named target. The blockade squeezes Iran. The closed or restricted strait squeezes Gulf exporters. The lost flow raises prices for buyers. The price shock travels into ordinary budgets through fuel, freight, food, and electricity.

This is the hard moral texture of chokepoint politics. Each side can describe its pressure as necessary. Each side can point to a larger security concern. The costs leave the room where the decision is made.

The chokepoint gathers many systems into one width.

The Public Price of a Narrow Place

AP reported that Brent crude closed above $108 per barrel on Monday, about 50 percent higher than when the war began. EIA’s April outlook forecast a Brent peak of $115 per barrel in the second quarter of 2026 under its assumptions, with U.S. gasoline averaging more than $3.70 per gallon for the year and diesel averaging $4.80 per gallon.

Those forecasts may change. The direction of the stress is already visible.

Fuel is a public price. It is printed on tall roadside signs and paid by people who have no seat in the talks. Diesel is even more public, though less visible. It sits inside trucking rates, farm costs, construction bids, school-bus budgets, emergency services, grocery distribution, and municipal work. LNG is public in another way. When cargoes are scarce, power systems and industrial buyers compete with households through utility bills and government subsidies.

Fertilizer makes the chain more direct. Gulf energy exports support global fertilizer markets through natural gas, ammonia, urea, and sulfur. A shipping disruption that begins as a security crisis can become an agricultural cost problem, then a food price problem, then a political problem in countries far away.

The map misses that. A map shows the strait as a line of water. Prices show the strait as a shared dependency.

That shared dependency is easy to ignore during normal flow. Cargoes disappear into the background when schedules hold. Refineries run. Trucks move. Planes take off. Grocery shelves look ordinary. The system becomes visible again when it slows down.

There is a civic lesson in that visibility, but it is a plain one. Modern life is less weightless than it pretends to be. The internet can move instantly. Money can clear electronically. Contracts can be signed across continents. Oil, gas, grain, fertilizer, and spare parts need routes. Routes have widths. Widths have politics.

The strait becomes public when distant routes reach the table.

What Reopens With the Strait

If the strait reopens, the first images will likely be practical: tankers moving again, insurance costs settling, oil benchmarks easing, diplomats claiming progress, analysts adjusting forecasts.

That would matter. A reopened passage would reduce immediate pressure on consumers, exporters, importers, and crews stuck in the wrong place at the wrong time. It would give governments room to breathe. It would allow some production to return and some prices to soften.

Reopening would leave the larger lesson intact.

Hormuz is a standing argument against any fantasy that energy security can be reduced to slogans about independence, dominance, or transition. Fossil-fuel dependence creates exposure to physical routes and producer politics. Clean-energy buildouts create other exposures: minerals, factories, transmission lines, ports, permits, and storage. Every energy system has material constraints. The public question is how honestly a society names them, pays for them, and spreads the burden when they fail.

The strait is also a reminder that low cost and security are different virtues. Low cost likes concentration, speed, and full use. Security likes slack, optionality, and redundancy. Most countries want both and pay fully for neither. They discover the gap when a narrow place becomes a price.

The ships waiting near Hormuz are carrying more than cargo. They are carrying a message about the shape of the world beneath the abstractions. A sea lane can become a negotiating table. A blockade can become a grocery bill. A diplomatic phrase can become diesel. And a strip of water 29 nautical miles wide can hold more of public life than any map has room to admit.