Who’s Really Funding Terror?

Inside Treasury’s 2024 Terrorist Financing Risk Assessment

Every few years, the U.S. Treasury Department drops a long, serious PDF that almost nobody outside government reads.

No viral thread, no cable news segment, just a link on a federal website.

This report quietly shapes what your bank flags as “suspicious,” how charities move money overseas, and how financial privacy is balanced against national-security monitoring every few years.

The report does three main things

It says the main terrorism danger to people inside the United States comes from individuals here at home, often inspired by extremist ideologies rather than directed by foreign groups. It highlights old and new money channels, including banks, cash, money transmitters, charities, virtual assets, and crowdfunding, as the places where terrorist funds are most likely to flow. And it builds everything on a mostly qualitative view of risk: who is dangerous, where the financial system is weak, and what happens when those two line up.

What is this report, in plain English?

Treasury publishes national risk assessments on three big topics: money laundering, terrorist financing, and weapons proliferation financing.

They’re the government’s top-level map of how dirty money moves through the financial system.

The terrorist financing risk assessment tries to answer one simple question

Who is raising and moving money for terrorism in or through the United States, where are the weak spots, and which combinations are most troubling?

The 2024 report answers that question by looking at three things

The assessment separates threats, which groups and individuals are active or inspiring others; vulnerabilities, where the financial system is easiest to abuse; and consequences, what happens when that mix goes wrong through attacks, recruitment, propaganda, and related harms.

Who is this report for?

On paper, the target audience is federal agencies, law enforcement, and financial supervisors who have to decide where to focus their attention.

In practice, it’s also a useful window for anyone trying to understand where “national security” meets “financial regulation.”

How Treasury thinks about risk

Treasury’s risk logic is pretty straightforward.

{kind=link}

The report asks:

Who might pose a danger?

Where are the weak points that make funding easier?

How bad would it be if those weak points are exploited?

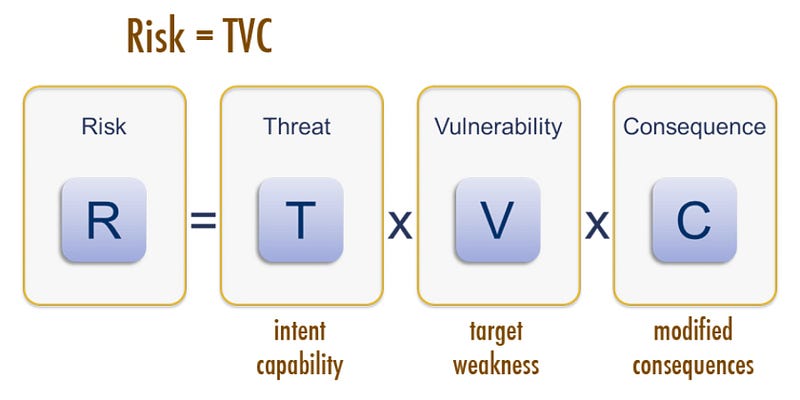

In formal terms, risk is treated as a mix of threat, vulnerability, and consequence:

Threats are terrorists, supporters, or networks that try to raise, move, or store money in or through the U.S. financial system.

Vulnerabilities are gaps in laws, controls, or business models that make that easier.

Consequences are the harm that follows if they succeed.

Treasury defines the problem, describes possible harms, talks about patterns and likelihood in broad terms, and pulls it all into a unified picture that decision makers can use.

Treasury punts on any kind of quantitative analysis or specific estimation of risk.

You won’t find probabilities, dollar-value loss estimates, or neat scorecards ranking every threat from 1 to 10.

What you get instead is a structured judgment: a narrative that compares threats and sectors in relative terms: higher concern, lower concern, growing concern.

For something as political and emotionally loaded as terrorism, that may be the only type of analysis you can publish while keeping the discussion grounded.

Who Treasury thinks is dangerous right now

So who does Treasury see as the biggest threat today?

The report is pretty direct on one point: the primary terrorism threat to the U.S. homeland comes from individuals inside the country, often radicalized online or through social networks.

Domestic violent extremists, especially racially or ethnically motivated violent extremists, are described as posing the most consistent threat of both lethal and non-lethal violence.

Foreign terrorist organizations remain on the radar. The assessment spends time on ISIS affiliates and al-Qa’ida, which continue to inspire plots and fundraising even when they aren’t directing operations.

The report also discusses Hizballah, Hamas, and other Iran-backed groups, which have built sophisticated financial networks mixing charities, front companies, and state support.

The October 2023 Hamas attacks sit in the background of this whole discussion.

Treasury treats that episode as a case study in what can happen when a group is allowed to build a complex financial operation over time and the danger is misread.

Treasury later described one related enforcement action in its release on sham overseas charity networks funding Hamas and the PFLP .

One uncomfortable truth runs through the report

Terrorist attacks often do not cost very much money.

A lone actor, an independent cell, can cause huge human harm with relatively modest funding.

That creates a nasty problem for regulators and compliance teams.

You can’t just watch the biggest money flows and assume you’re covering the most serious threats.

Where the money moves: banks, charities, apps, and crypto

For people in finance, compliance, and the non-profit world, the most concrete part of the report is the discussion of channels.

Channels are the places where terrorist funds are most likely to show up.

Banks and money services

Traditional payment channels move a lot of volume.

Banks, wire services, and other money transmitters are central to risk and detection.

Between 2020 and 2022, registered money services businesses filed the majority of suspicious activity reports tied to terrorist financing. That’s a pretty strong hint about where a lot of concerning patterns show up first.

Cash and informal transfer systems matter as well, especially for cross-border movement and for people trying to stay off the radar.

Charities and non-profits

Non-profits are always a sensitive topic in this space. They send money into fragile regions where terrorist groups also operate. They also provide real relief and social services to people in extreme need.

Treasury tries to walk a careful line.

The report stresses that most U.S. charities have little exposure to terrorist financing, while acknowledging that a small subset, especially some international charities and outright sham groups, can be misused. Treasury’s framing keeps the focus on specific risk patterns instead of treating the whole sector as suspicious by default.

Virtual assets and online fundraising

Compared with earlier editions, the 2024 assessment spends more time on virtual assets and crowdfunding.

Terrorist groups and their supporters have experimented with public crypto donation drives, mixers and other privacy tools, and online crowdfunding campaigns pitched as humanitarian or political causes.

Treasury does not claim that crypto is now the main way terrorists get money. Banks, cash, and money transmitters remain dominant, but the report clearly sees virtual assets and crowdfunding as fast-moving zones where risk can grow quickly if controls lag behind new business models.

If you run a crypto platform or payment app, the message is simple: you are on the radar, and you’re expected to understand your exposure.

Strengths and gaps in Treasury’s approach

Read strictly as a risk assessment, the 2024 report gets a lot right.

Strengths

It is clear about its purpose and how it fits with other national reports on illegal finance. Terrorist financing is presented as one piece of a broader picture, not a stand-alone obsession.

It uses a consistent way of organizing the problem, threats, vulnerabilities, and consequences, and sticks with that structure from start to finish.

It connects directly to real decisions: where to focus investigations, which sectors deserve closer supervision, and how to shape national priorities for anti-money-laundering and counter-terrorist-financing work.

Gaps

First, the guiding question is broad.

The report promises to “identify threats, vulnerabilities, and risks” to the U.S. financial system. That description is accurate, but wide open. If you need to decide whether to put more staff on examining money transmitters or more money into tracing virtual assets, you need more analysis.

Second, the risk picture is almost entirely qualitative.

The language leans on phrases like “primary threat,” “most pressing,” and “limited exposure.” Those terms carry meaning, and Treasury backs some of them with straightforward indicators like suspicious report shares or investigation trends. But you will not find probabilities, dollar figures, or a ranking table that clearly orders one sector above another.

Third, uncertainty gets limited airtime.

The report admits that data are incomplete, that new technologies move fast, and that small sums can produce large human harm. What it does not really do is spell out where its own judgments are strongest, where they’re weaker, or how new information might change the picture.

From a technical risk-analysis perspective, those are all real limitations.

From a political perspective, they might be intentional.

It’s hard to imagine a public document that puts numeric odds on different types of terrorist attacks and survives contact with Congress or cable news.

Why this matters

If you work in finance or fintech, documents like this shape what regulators expect from your risk assessments, your monitoring systems, and your compliance budget. When Treasury says money transmitters see most of the suspicious reports tied to terrorist financing, or that certain crowdfunding patterns are showing up more often, that is a signal about where examiners will look.

If you work in the non-profit world, especially internationally, reports like this affect how banks view your accounts. The message that most charities are low risk, but a small slice are higher risk, is the tension you live inside every time a wire transfer gets held up for “review.”

If you work in policy, the NTFRA is one more proof point that the United States has fully leaned into a risk-based approach to financial crime. The goal is not to eliminate all terrorist financing. That is not realistic. The goal is to understand where the danger is concentrated and push scarce resources in that direction.

So if I had to give the 2024 Terrorist Financing Risk Assessment a grade, I’d call it an A.

Not because it answers every question or settles every argument, but because it offers a clear, structured story about who Treasury sees as today’s main terrorist threats, how those actors are trying to raise and move money, where the U.S. financial system is most exposed, and where new cracks may be forming.

For a 100-plus-page government PDF that most people will never open, that’s a lot of information hiding in plain sight.

Sources checked

- U.S. Treasury, 2024 National Terrorist Financing Risk Assessment .

- U.S. Treasury, 2024 national risk assessments press release .

- Congressional Research Service, Hamas October 2023 attacks background .